The State of Climate Action in 2025: 10 key findings

Sophie Boehm* and Clea Schumer, with research contributions from Joel Jaeger, Yuke Kirana, Kelly Levin, Raychel Santo, Katie Lebling, Danielle Riedl, Anderson Lee, Neelam Singh, Michelle Sims, Neil Chin, Aman Majid, Sarah Cassius, Will Lamb, Ankita Gangotra, Neil Grant, Yiqian Zhang-Billert, and Michael Petroni.

The 2025 State of Climate Action report is sobering: Not one of the 45 indicators assessed is on track to achieve its 2030 target. Unprecedented transformational changes across every sector are needed to keep the Paris Agreement goal within reach.

Share

This year marks the 10th anniversary of the Paris Agreement, a watershed moment on climate action when more than 190 countries agreed to pursue efforts to limit global warming to 1.5 degrees C (2.7 degrees F) above pre-industrial levels. Achieving this goal can not only help avoid increasingly catastrophic climate impacts, but also secure countless benefits — from advancing energy security, to improving human health and well-being, to protecting ecosystems that deliver life-sustaining services.

The 2025 State of Climate Action report, the fifth in the series, is sobering: Not one of the 45 indicators assessed is on track to achieve its 2030 target.

Here are 10 key takeaways from this year’s report card, ranging from some of the most promising signs of progress to areas lagging far behind.

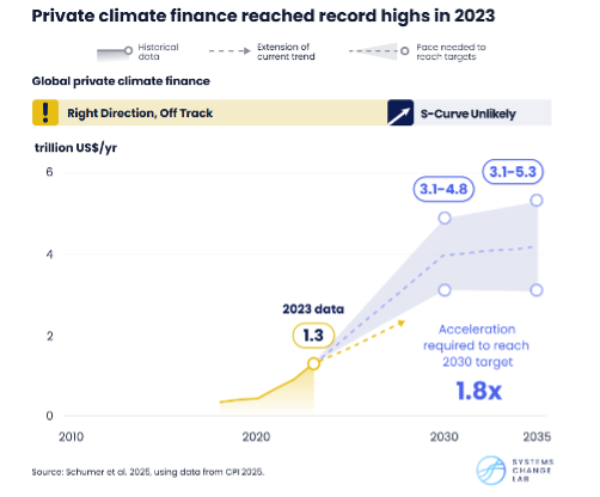

1. Private climate finance increased so sharply that global efforts to mobilize these funds shifted from “well off track” to just “off track.”

Between 2022 and 2023, climate finance from the private sector rose from roughly $870 billion to a record high of $1.3 trillion, and early estimates for 2024 suggest continued momentum. Individual consumers, businesses and institutional investors, particularly in China and western Europe, drove much of these recent gains.

Although still off track to reach at least $3.1 trillion by 2030, this jump invites optimism. Private climate finance is already enabling the scale-up of existing zero-carbon technologies, such as electric vehicles and heat pumps. And when pooled with public funds, it can accelerate deployment even further, as well as help nurture innovation and first-of-a-kind ventures.

Still, private capital alone will not be enough. All sources of finance need to be urgently aligned with the Paris Agreement and mobilized at scale to help transform all sectors. Dramatically scaling up public climate finance is critical, especially in areas where the private sector is currently unwilling or poorly positioned to invest due to high perceived risk or low expected returns. Restoring the world’s forests, expanding public transit infrastructure and developing climate-smart agricultural technologies, for example, have attracted disproportionately fewer investments from private funders.

2. Relatively new innovations, like green hydrogen, technological carbon dioxide removal and electric trucks, also saw some of the most meaningful one-year gains.

Although not yet close to mainstream breakthrough, these technologies experienced impressive advances in 2023 and 2024 that, if sustained, could be an early signal of acceleration ahead. For example, green hydrogen production more than quadrupled in a single year. And the share of electric trucks in medium- and heavy-duty commercial vehicle sales rose by 67% between 2023 and 2024.

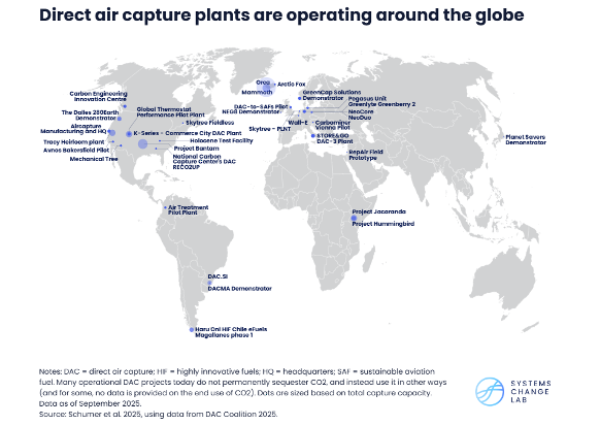

Similarly, over 30 direct air capture projects are operating around the world today, and many more are in development. By one estimate, another 50 facilities could come online in the near future, including three that may each capture upwards of 500,000 tonnes of CO2 (tCO2) annually — nearly 14 times more than the capture capacity of today’s largest plant. But while promising and fast-growing, direct air capture currently accounts for a relatively small share of technological dioxide carbon removal. Getting on track for 2030 will require scaling up all novel approaches more than 10 times faster. To put this into perspective, this is roughly equivalent to building nine of the largest direct air capture facilities currently in development each month through the end of this decade.

Measures to stimulate greater demand for these innovations, as well as investments in their development and deployment, will prove critical to ensuring that these recent gains in adoption translate into longer-term momentum.

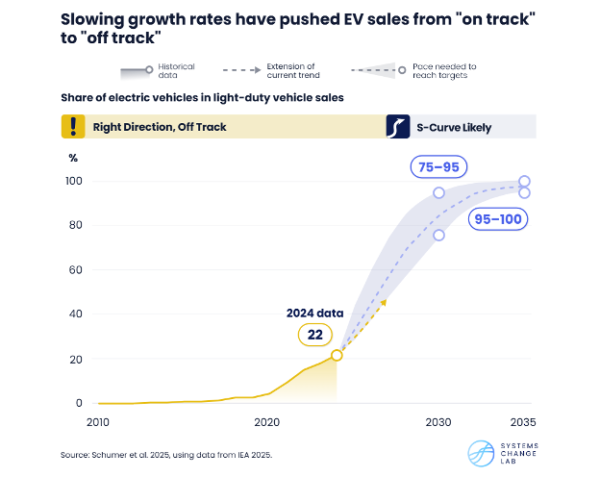

3. Electric vehicle sales are still rising, but slowdowns in some major markets have pushed progress from “on track” to “off track.”

Global EV sales have continued to rise rapidly, reaching a record 22% of global passenger car sales in 2024 compared to just 4.4% in 2020. Much of this growth has been driven by China — the world’s leading EV consumer and manufacturer — where nearly half of all passenger cars sold are now electric.

But in two other major markets, momentum has stalled. EV sales fell slightly in Europe following the rollback of supportive subsidies in countries like Germany and France. In the United States, growth in EV sales has decelerated due to a combination of factors, including a relatively slow buildout of public charging infrastructure and limited availability of affordable electric SUVs, which account for three-quarters of America’s passenger car sales.

Consequently, the rate at which EVs are growing as a share of total light-duty vehicle sales fell to an average of roughly 20% per year in 2023 and 2024, compared to more than 60% in the previous three years. While still remarkable, these recent gains lag behind what’s needed to help achieve the Paris Agreement’s temperature goal. This marks a downgrade from the last State of Climate Action, when EV sales were the only indicator on track.

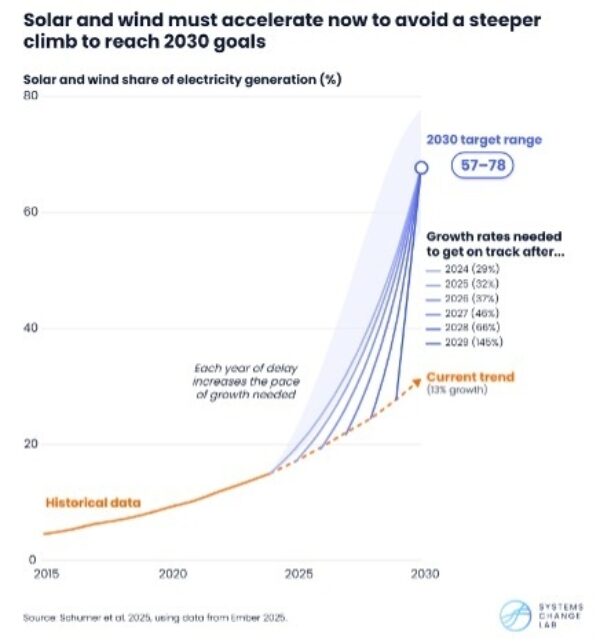

4. Solar and wind keep hitting new milestones, but sustaining current growth rates won’t be enough to get on track for 2030.

Solar power is the fastest growing source of electricity in history, repeatedly exceeding projections for future increases in installed capacity and generation. Today, solar around the world generates roughly 2,100 terawatt-hours each year — roughly 8 times more than in 2015 and 66 times more than in 2010. And in 2024 alone, countries collectively added enough solar power to the grid to meet the equivalent of France’s entire electricity demand that year.

Together, the share of solar and wind in electricity generation has grown at an average rate of roughly 13% per year since 2020. But while this relatively consistent growth is impressive, maintaining this trajectory won’t be enough to get on track for 2030. Instead, solar and wind need to grow more than twice as fast, at 29% per year — and delays only make the challenge steeper.

This underscores a critical reality for all indicators assessed. Every year that passes in which current growth rates are sustained, rather than accelerated, increases the magnitude of the acceleration that is needed thereafter. Only by substantially picking up the pace of change can the world make up for delayed efforts and moving another year close to 2030.

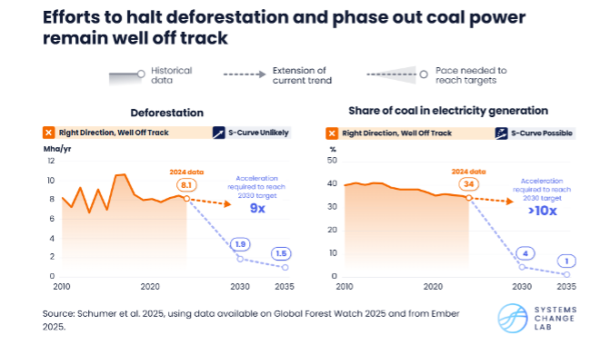

5. The world has barely moved the needle on some of the most important climate actions, like phasing out coal and halting deforestation.

Sharply reducing deforestation is crucial to halting climate change. The world’s forests hold roughly 870 gigatonnes of carbon (GtC) — nearly twice the amount emitted from fossil fuels since 1850. At least a third of these carbon stocks (around 280 GtC) are vulnerable to human disturbances, meaning they would be immediately released if forests are converted to pasturelands or croplands. Once lost, much of this carbon would be difficult for forests to recover in time to help reach net zero by mid-century.

Yet despite the outsized role that protecting these ecosystems can play in avoiding future GHG emissions, efforts to effectively halt deforestation remain well off track for the third State of Climate Action in a row. Although permanent forest loss dropped from a record high of 10.7 million hectares per year (Mha/yr) in 2017 to 7.8 Mha/yr in 2021, it has since ticked upward to reach 8.1 Mha/yr in 2024. This is roughly equivalent to losing nearly 22 football (soccer) fields of forests per minute — permanently. This recent spike in deforestation has dampened a longer-term downward trend observed since 2015, such that getting on track for 2030 will now require the rate of permanent forest loss to decline nine times faster.

Equally concerning are sluggish efforts to phase out coal — by far the largest source of GHG emissions in the power sector. As a share of global electricity generation, coal fell only slightly from 37% in 2019 to 34% in 2024 and remains “well off track” for the fourth consecutive report.

Keeping the Paris Agreement limit within reach will require coal-fired power to decline more than 10 times faster, reaching just 4% by 2030. This is roughly equivalent to retiring nearly 360 average-sized coal-fired power plants each year through the end of this decade, as well as halting all planning for and development of new coal capacity currently in the pipeline. Continued delays also risk stymying mitigation efforts across buildings, industry and transport, which all rely on electrification and a decarbonized power grid to reduce GHG emissions.

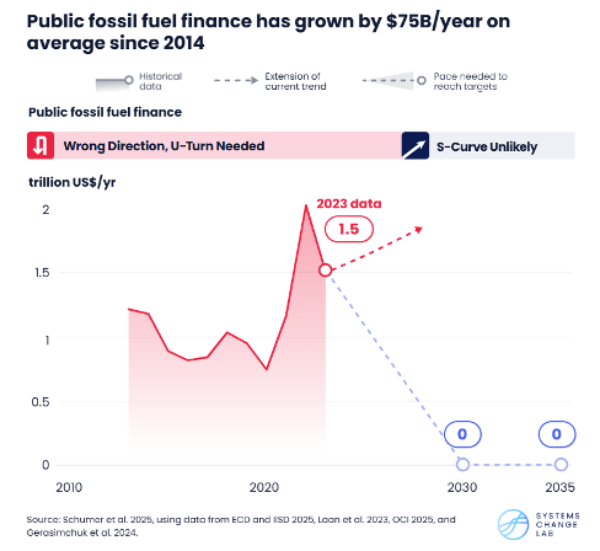

6. Public finance for fossil fuels is still climbing, despite global pledges to phase out subsidies.

The world has seen a troubling rise in public finance for oil, gas and coal precisely when these investments need to be declining steeply. Since 2014, governments’ financial support for fossil fuels — such as production and consumption subsidies and funding from domestic and international development finance institutions — has increased by an average of roughly $75 billion per year.

While these investments did fall from an all-time high of $2.1 trillion in 2022 to $1.5 trillion in 2023, much of this one-year drop can be attributed to falling international oil and gas prices, which led to a reduction in public funds subsidizing the consumption of fossil fuels like gasoline. Critically, these subsidies represent the largest form of government support for fossil fuels and generally ebb and flow alongside fluctuations in oil and gas prices. This most recent decline, then, represents limited progress at best. A step-change in action will be needed to phase out public financial support for fossil fuels by 2030.

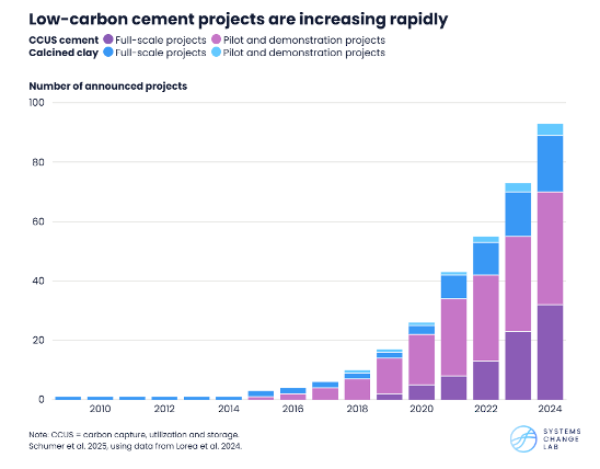

7. Progress on decarbonizing emissions-intensive steel and cement production is a mixed bag.

Steel and cement serve as the building blocks of our cities, homes and workplaces. They are also among the most emissions-intensive materials to produce, and — given the high temperatures required to make them and their substantial “process emissions” (GHGs emitted from chemical reactions during production) — are some of the hardest to decarbonize via existing approaches, like electrification.

Since 2018, the carbon intensity of global steel production has increased. This is a particularly worrying trend, given that steel alone is responsible for upwards of 7% of global CO2 emissions. Solutions exist to help steelmakers change course; for example, reusing more “scrap” steel, swapping out coal and fossil gas for green hydrogen, and shifting to electric furnaces. But these are not yet readily available. Green hydrogen, while growing rapidly, remains relatively nascent and expensive, while quantities of recycled or “scrap” steel are limited.

Global efforts to decarbonize cement are slightly more promising. The State of Climate Action 2023 found that progress had stagnated and needed to occur more than 10 times faster to get on track for 2030. Since then, the amount of CO2 emitted per tonne of cement produced has begun to decline thanks to energy efficiency gains; greater use of alternative low-carbon fuels; and increased substitution of clinker (the primary component of cement) for less emissions-intensive materials, like calcined clay. Now, getting on track for 2030 requires a fourfold acceleration. Encouragingly, the past five years have seen a surge in new projects focused on decarbonizing cement production, signaling that the world is paying more attention to addressing this challenge.

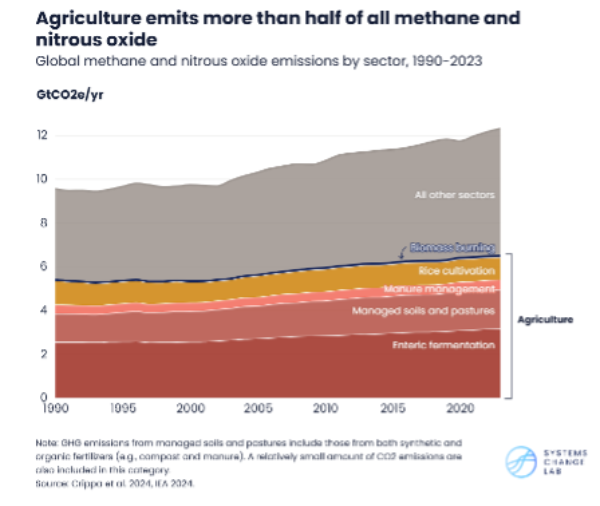

8. Promising solutions are emerging in agriculture to tackle some of the world’s most potent GHG emissions — but efforts to scale them are coming up short.

Agricultural production accounts for roughly half of global methane and nitrous oxide emissions, which have far more warming power than CO2, particularly in the near term. Major sources include enteric fermentation (the process by which some livestock release methane as they digest); the application of both synthetic and organic fertilizers, like manure and compost; rice production; and manure management.

While these absolute emissions have risen slowly but steadily since 2000, recent years have seen the emissions intensity of agriculture (the amount of GHGs released per kilocalorie of food produced) decline across all major sources. Now, getting on track for 2030 will require these improvements to occur 1.2 times faster for fertilizers, 2.5 times faster for enteric fermentation, and 6 times faster for both manure management and rice cultivation.

Yet accelerating progress is no small feat. Compared to the power sector — where solar and/or wind power can be deployed almost anywhere — there’s not an equivalent, predominant solution to reducing emissions from agriculture. Rather, technologies and practices must be tailored to each context, considering factors like the local climate, soil conditions, crop varieties, livestock breeds, agricultural traditions and more.

That said, a variety of promising strategies are available, but have yet to be adopted at scale. A well-established method of repeatedly flooding and drying rice paddies, for example, has significantly reduced methane emissions from rice production within a handful of Asian countries. Meanwhile, introducing easier-to-digest feeds has lowered enteric fermentation emissions across much of Europe and North America. More concerted efforts and financial support are urgently needed to bring — and adapt — these strategies to the regions that need them most.

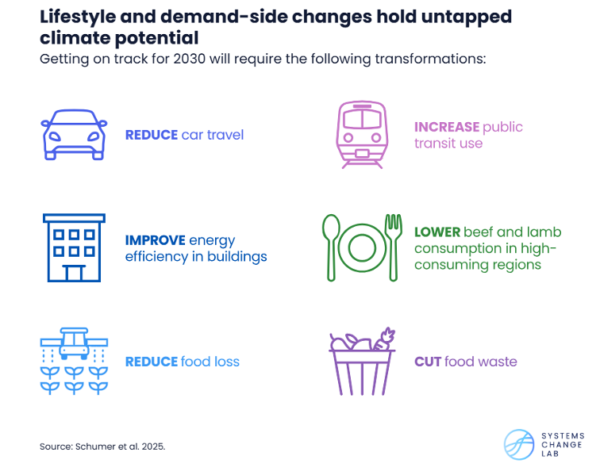

9. Shifting demand — for example, across diets, transit networks and buildings — can deliver substantial emissions reductions, but these changes have yet to take off.

The IPCC finds that shifting consumption patterns, particularly among the world’s highest-earning households, can reduce GHG emissions 40%-70% by 2050 when compared with current climate policies. Cycling, walking or taking public transit instead of driving; avoiding long-haul flights; adopting more plant-rich diets; cutting food waste; and improving energy efficiency in our homes and workplaces are among the most effective changes.

Yet these global transitions have largely stalled. The share of trips taken by private passenger cars, most of which still rely on gasoline, continues to increase and now accounts for about half of all kilometers traveled — despite progress in expanding bicycle lanes and public transit networks among the world’s most populous cities. Energy efficiency improvements in buildings (as approximated by the amount of energy consumed per square meter of floor area) have also slowed in recent years. And available evidence suggests the world has made almost no dent in halving food loss and waste by 2030.

Meanwhile, per capita consumption of beef, lamb and goat meat across high-consuming regions has decreased slightly, from 107 kilocalories per day in 2018 to 104 kilocalories per day in 2022. But it needs to fall to no more than 79 kilocalories per person per day by 2030. This will entail the average person eating about 1.9 fewer servings per week in Australia and New Zealand, 1.3 fewer servings per week in South America and 1.2 fewer servings per week in North America. Fortunately, several initiatives are underway to make protein-rich beans, lentils and other legumes more accessible and appealing. And public investments have grown to support the research, development and deployment of alternative proteins, like plant-based and cultivated meats.

Supportive policies — including measures that incentivize efficiency improvements and help make sustainable behaviors the easiest, most affordable options — can help accelerate these shifts.

10. Persistent data limitations across some sectors mean we still can’t fully assess global climate action.

For a handful of indicators, particularly those focused on decarbonizing buildings and conserving wetland ecosystems, data has been insufficient to assess progress for every installment of the State of Climate Action series. This includes some that could deliver substantial reductions in GHG emissions.

Peatlands, for example, cover just 3.8% of Earth’s land, but contain at least a fifth of the world’s soil organic carbon stocks and store an order of magnitude more carbon per hectare than forests. Once degraded, these ecosystems can emit CO2 and nitrous oxide for decades to centuries until all peat is fully lost or their soils are rewetted. Accordingly, halting peatland degradation and restoring 15 million hectares of degraded peatlands by 2030 can offer immediate and relatively large reductions in GHG emissions. But despite recent progress in mapping these ecosystems, efforts to monitor annual changes in peatlands’ extent are insufficient to grade progress. Without better data, the world has very limited insights on whether we are losing or recovering these vital carbon hotspots.

Toward a more prosperous and sustainable future

Unprecedented transformational changes across every sector, alongside large-scale carbon removal, are needed immediately to keep the Paris Agreement goal within reach. But despite some pockets of progress, such as rapid growth in EV sales and renewable power, climate action across the board continues to fall far short of what’s needed.

In spite of these grave challenges — indeed, precisely because global progress lags so far behind — achieving Paris-aligned targets for 2030 is all the more vital. Should warming exceed 1.5 degrees C even temporarily, already devastating impacts will only intensify, subjecting more people to increasingly frequent and severe storms, longer heatwaves and droughts, more extreme flooding and sea level rise, and more. Overshooting this threshold of warming also increases the likelihood that these future risks will compound one another, with multiple hazards battering communities at the same time.

Every fraction of a degree matters for lessening the scale and severity of these impacts. And the roadmap for reducing GHG emissions and enhancing carbon removals is clear: Everything from phasing out unabated fossil gas to electrifying industry is urgently required this decade — and remains technically feasible.

In this eleventh hour, we still have time to course correct. There’s no sugar-coating the fact that the challenge ahead is immense, and the scale of change required is unprecedented. But just because something is unprecedented doesn’t mean it’s impossible. The solutions exist. We know what to do. We just need to act with the urgency this moment demands.

This article focuses on the 2025 findings of the annual State of Climate Action report series. View past articles here: 2023 | 2022 | 2021 | 2020.